We are committed to providing accurate content that helps you make informed money decisions. Our partners have not commissioned or endorsed this content. Read our editorial guidelines here.

There are hundreds of metros in the U.S., but the 50 with the largest populations — including places like New York, Los Angeles and Chicago — often get disproportionate attention. Yes, these heavily populated metros can be great for homeowners, but others are also worth considering.

With that in mind, LendingTree studied often-overlooked metros. Specifically, we used U.S. Census Bureau data to examine 142 metros that have populations of at least 250,000, but are too small to be among the nation’s 50 largest. We ranked them based on six categories:

- Median home value

- Homeownership rate

- Median household income of owner-occupied homes with a mortgage

- Median monthly housing costs of owner-occupied homes with a mortgage

- Share of owner-occupied homes with a mortgage that spend less than 30% of their monthly income on housing costs

- Median annual property taxes for homes with a mortgage

Here are the top 50 metros (chosen from the 142) that are hidden gems for homeownership.

On this page

Key findings

- Huntsville, Ala., Charleston, W.Va., and Fort Wayne, Ind., are the three best hidden gem metros for homeownership. Huntsville and Fort Wayne have the highest and second-highest share of homes that spend less than 30% of their income on housing costs, while Charleston has the second-lowest median monthly housing costs and third-lowest median home value.

- Metros in three states with relatively low costs of living — West Virginia, Indiana and Ohio — take up seven of the 10 best hidden gem metros for homeownership. Two West Virginia metros — Charleston (second) and Huntington (fourth) — two Ohio metros — Youngstown (seventh) and Canton (10th) — and three Indiana metros — Fort Wayne (third), South Bend (fifth) and Evansville (ninth) — appear in our study’s top 10.

- All 50 of the metros highlighted can be solid for homebuyers. While we only included 50 metros, we looked at 142 when determining the nation’s hidden gems. Because of this, even metros that just cracked the top 50 — like Des Moines, Iowa (50th), Rochester, N.Y. (49th), and Baton Rouge, La. (48th) — can be great for house hunters to consider making their home.

Top hidden gem metros for homeownership

No. 1: Huntsville, Ala.

- Population: 502,728

- Median home value: $246,000

- Homeownership rate: 71.25%

- Median household income of owner-occupied homes with a mortgage: $105,012

- Median monthly housing costs of owner-occupied homes with a mortgage: $1,305

- Share of owner-occupied homes with a mortgage that spend less than 30% of their monthly income on housing costs: 84.58%

- Median annual property taxes for homes with a mortgage: $881

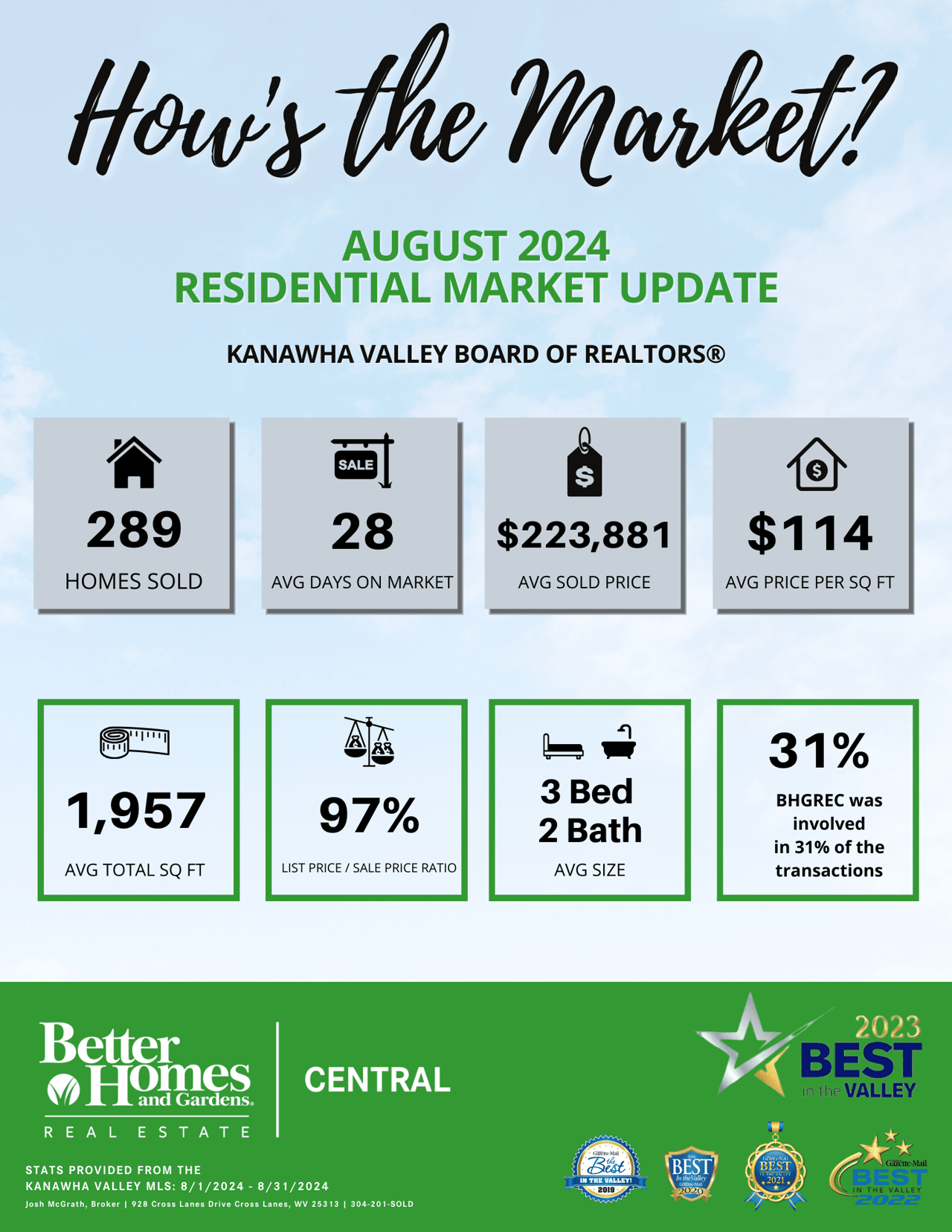

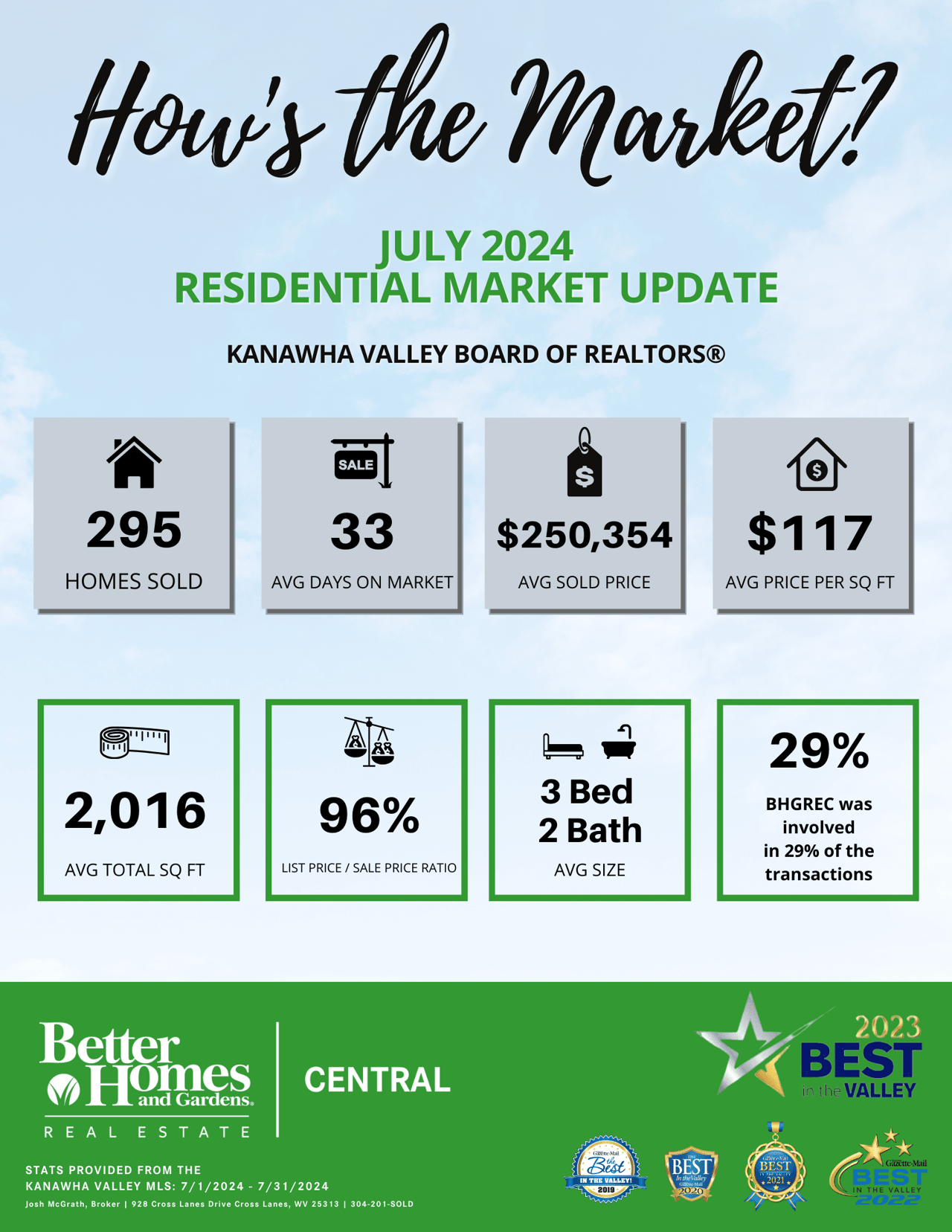

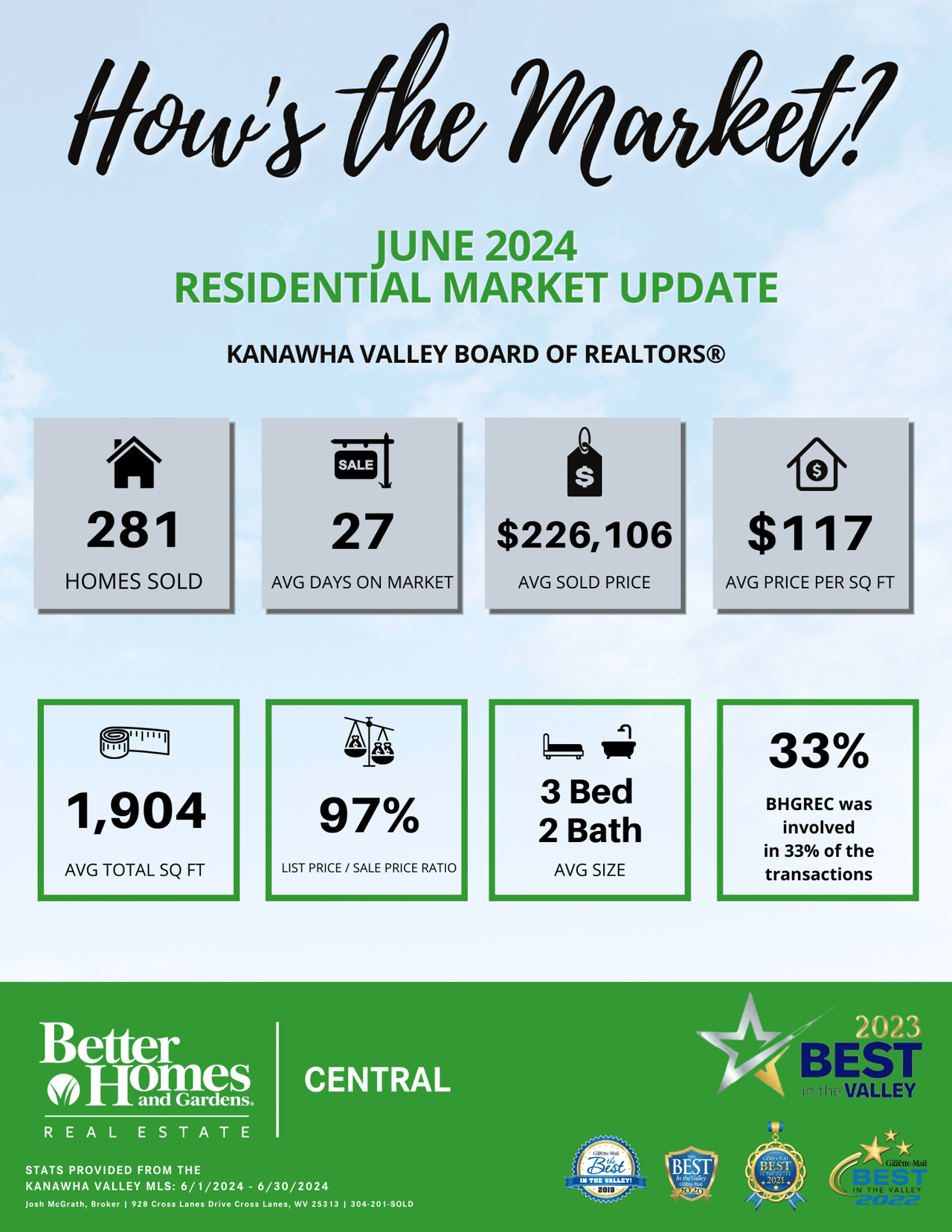

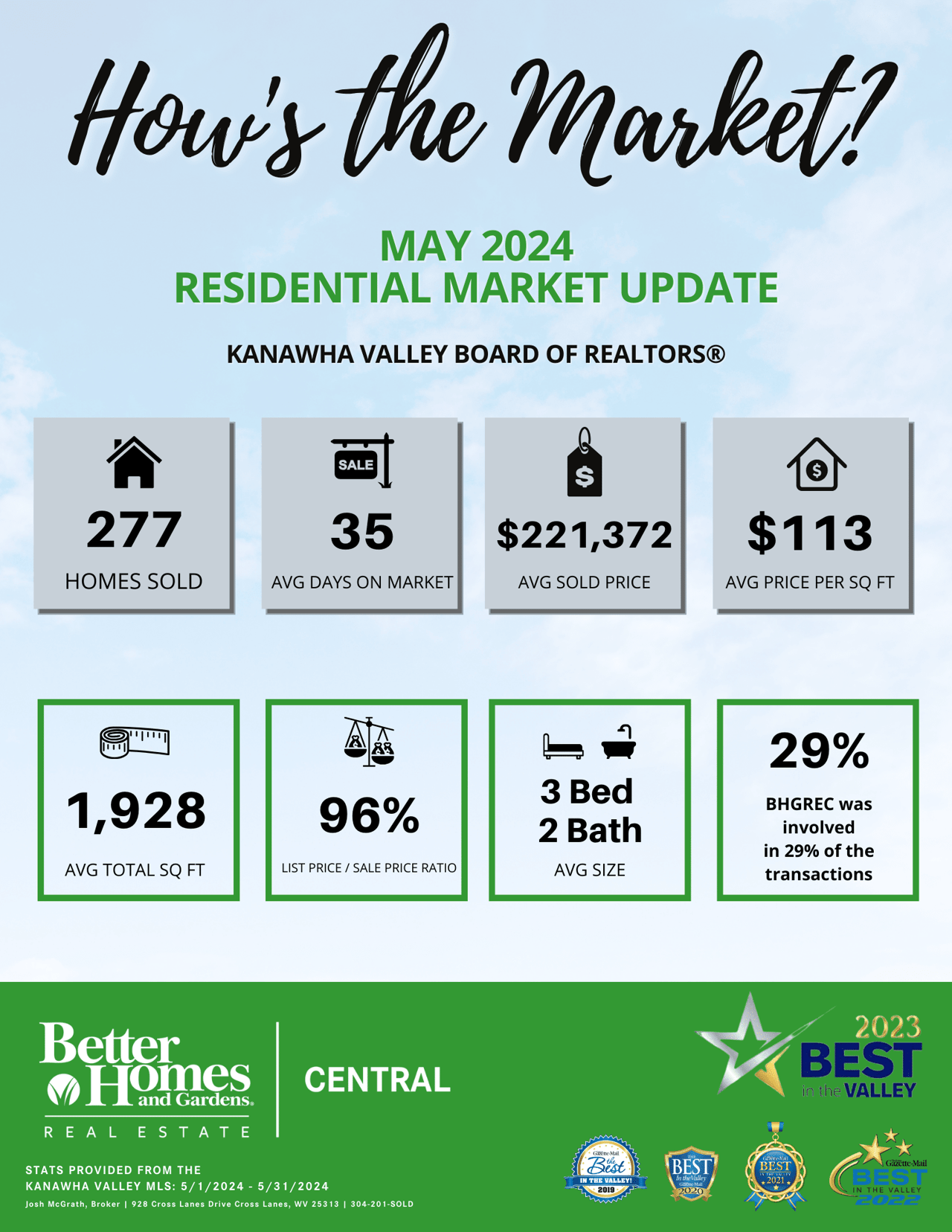

No. 2: Charleston, W.Va.

- Population: 252,942

- Median home value: $124,600

- Homeownership rate: 71.97%

- Median household income of owner-occupied homes with a mortgage: $78,369

- Median monthly housing costs of owner-occupied homes with a mortgage: $1,074

- Share of owner-occupied homes with a mortgage that spend less than 30% of their monthly income on housing costs: 77.44%

- Median annual property taxes for homes with a mortgage: $910

No. 3: Fort Wayne, Ind.

- Population: 423,038

- Median home value: $173,000

- Homeownership rate: 70.98%

- Median household income of owner-occupied homes with a mortgage: $82,791

- Median monthly housing costs of owner-occupied homes with a mortgage: $1,104

- Share of owner-occupied homes with a mortgage that spend less than 30% of their monthly income on housing costs: 84.25%

- Median annual property taxes for homes with a mortgage: $1,364

No. 4: Huntington, W.Va.

- Population: 356,581

- Median home value: $130,700

- Homeownership rate: 73.50%

- Median household income of owner-occupied homes with a mortgage: $78,933

- Median monthly housing costs of owner-occupied homes with a mortgage: $1,106

- Share of owner-occupied homes with a mortgage that spend less than 30% of their monthly income on housing costs: 76.54%

- Median annual property taxes for homes with a mortgage: $1,110

No. 5: South Bend, Ind.

- Population: 323,695

- Median home value: $163,700

- Homeownership rate: 71.94%

- Median household income of owner-occupied homes with a mortgage: $82,628

- Median monthly housing costs of owner-occupied homes with a mortgage: $1,123

- Share of owner-occupied homes with a mortgage that spend less than 30% of their monthly income on housing costs: 79.22%

- Median annual property taxes for homes with a mortgage: $1,548

Full ranking: Hidden gem metros for homeownership

| Rank | Metro | Population | Median Home Value | Homeownership Rate | Median Household income of owner-occupied homes with a mortgage | Median monthly housing cost of owner-occupied homes with a mortgage | Share of owner-occupied homes with mortgage spending less than 30% of their monthly housing cost | Median annual property taxes for homes with a mortgage |

| 1 | Huntsville, AL | 502,728 | $246,000 | 71.25% | $105,012 | $1,305 | 84.58% | $881 |

| 2 | Charleston, WV | 252,942 | $124,600 | 71.97% | $78,369 | $1,074 | 77.44% | $910 |

| 3 | Fort Wayne, IN | 423,038 | $173,000 | 70.98% | $82,791 | $1,104 | 84.25% | $1,364 |

| 4 | Huntington, WV | 356,581 | $130,700 | 73.50% | $78,933 | $1,106 | 76.54% | $1,110 |

| 5 | South Bend, IN | 323,695 | $163,700 | 71.94% | $82,628 | $1,123 | 79.22% | $1,548 |

| 6 | Spartanburg, SC | 335,864 | $193,300 | 74.50% | $81,250 | $1,180 | 81.06% | $1,303 |

| 7 | Youngstown, OH | 538,069 | $131,200 | 71.22% | $78,596 | $1,049 | 80.05% | $1,941 |

| 8 | Hickory, NC | 366,441 | $174,600 | 71.47% | $76,710 | $1,079 | 78.43% | $1,248 |

| 9 | Evansville, IN | 313,946 | $168,100 | 68.83% | $82,925 | $1,184 | 79.16% | $1,328 |

| 10 | Canton, OH | 400,525 | $162,400 | 69.60% | $82,548 | $1,140 | 80.37% | $2,150 |

| 11 (tie) | Lynchburg, VA | 263,571 | $207,700 | 72.41% | $84,125 | $1,231 | 76.81% | $1,135 |

| 11 (tie) | Peoria, IL | 398,473 | $141,700 | 73.69% | $86,803 | $1,233 | 78.78% | $3,231 |

| 13 | Knoxville, TN | 893,002 | $232,100 | 69.79% | $89,566 | $1,280 | 79.23% | $1,234 |

| 14 | Greenville, SC | 940,774 | $221,400 | 71.92% | $87,361 | $1,270 | 77.82% | $1,299 |

| 15 | Duluth, MN | 292,285 | $191,900 | 73.95% | $91,689 | $1,344 | 78.08% | $2,219 |

| 16 | Davenport, IA | 381,447 | $152,000 | 71.97% | $87,609 | $1,255 | 77.72% | $2,981 |

| 17 | Longview, TX | 287,868 | $155,700 | 71.28% | $90,057 | $1,251 | 74.84% | $2,410 |

| 18 | Scranton, PA | 567,750 | $159,100 | 68.41% | $89,188 | $1,271 | 78.45% | $2,580 |

| 19 | Kingsport, TN | 307,318 | $164,200 | 73.11% | $71,790 | $1,105 | 71.82% | $1,105 |

| 20 (tie) | Toledo, OH | 644,217 | $155,900 | 65.42% | $90,004 | $1,235 | 79.24% | $2,690 |

| 20 (tie) | Chattanooga, TN | 567,395 | $229,500 | 68.00% | $91,390 | $1,294 | 79.27% | $1,620 |

| 22 (tie) | Fayetteville, AR | 558,507 | $242,400 | 65.03% | $99,641 | $1,368 | 82.71% | $1,428 |

| 22 (tie) | Grand Rapids, MI | 1,091,620 | $245,300 | 74.52% | $94,362 | $1,354 | 80.50% | $2,792 |

| 24 | Harrisburg, PA | 596,305 | $219,000 | 70.96% | $101,971 | $1,454 | 79.50% | $2,883 |

| 25 | Winston-Salem, NC | 681,438 | $193,100 | 70.15% | $83,063 | $1,219 | 76.07% | $1,551 |

| 26 | Hagerstown, MD | 300,820 | $231,500 | 70.89% | $92,852 | $1,362 | 78.11% | $1,741 |

| 27 | Lafayette, LA | 479,212 | $181,000 | 69.46% | $82,808 | $1,237 | 73.86% | $1,149 |

| 28 | Erie, PA | 269,011 | $151,500 | 67.56% | $82,404 | $1,156 | 79.13% | $2,795 |

| 29 | Ocala, FL | 385,915 | $193,300 | 78.51% | $73,747 | $1,133 | 74.17% | $1,670 |

| 30 (tie) | Augusta, GA | 616,395 | $182,000 | 68.42% | $85,792 | $1,255 | 76.09% | $1,452 |

| 30 (tie) | Montgomery, AL | 386,814 | $160,000 | 65.09% | $79,709 | $1,214 | 75.64% | $562 |

| 32 (tie) | Beaumont, TX | 395,419 | $151,400 | 68.92% | $97,248 | $1,440 | 76.39% | $2,890 |

| 32 (tie) | Akron, OH | 700,015 | $181,700 | 67.76% | $91,516 | $1,302 | 79.73% | $2,901 |

| 34 | Springfield, MO | 479,598 | $194,100 | 65.49% | $80,167 | $1,181 | 77.98% | $1,430 |

| 35 | Greensboro, NC | 778,848 | $180,700 | 66.44% | $82,996 | $1,222 | 76.61% | $1,642 |

| 36 | Roanoke, VA | 315,442 | $220,900 | 69.10% | $88,977 | $1,307 | 77.07% | $1,788 |

| 37 | Columbia, SC | 836,324 | $185,800 | 69.67% | $81,880 | $1,242 | 73.39% | $1,273 |

| 38 | Gulfport, MS | 418,082 | $163,700 | 67.60% | $83,616 | $1,238 | 72.43% | $1,380 |

| 39 | Little Rock, AR | 749,673 | $183,700 | 64.31% | $86,496 | $1,253 | 76.47% | $1,341 |

| 40 | Dayton, OH | 813,516 | $169,300 | 65.74% | $89,977 | $1,259 | 78.12% | $3,006 |

| 41 | Utica, NY | 290,211 | $152,300 | 68.90% | $84,822 | $1,254 | 77.34% | $3,563 |

| 42 | Green Bay, WI | 329,490 | $225,300 | 68.82% | $98,024 | $1,406 | 80.79% | $3,272 |

| 43 | Lansing, MI | 540,281 | $179,200 | 67.81% | $88,954 | $1,291 | 77.72% | $2,912 |

| 44 | Cedar Rapids, IA | 275,435 | $180,700 | 76.45% | $86,124 | $1,361 | 75.83% | $3,053 |

| 45 | Ogden, UT | 708,543 | $395,400 | 75.14% | $104,555 | $1,602 | 77.60% | $2,170 |

| 46 (tie) | Flint, MI | 404,208 | $157,400 | 70.74% | $75,078 | $1,240 | 74.71% | $2,498 |

| 46 (tie) | Syracuse, NY | 658,281 | $164,000 | 68.07% | $95,799 | $1,414 | 78.68% | $4,475 |

| 48 | Baton Rouge, LA | 871,905 | $213,400 | 68.31% | $93,628 | $1,447 | 73.67% | $1,354 |

| 49 | Rochester, NY | 1,084,973 | $171,000 | 68.15% | $95,636 | $1,377 | 78.83% | $4,712 |

| 50 | Des Moines, IA | 719,146 | $229,900 | 69.35% | $102,350 | $1,518 | 80.90% | $4,003 |

Hidden gem metros can provide a good blend of affordability and opportunity

Looking for a new area to live in can be challenging. This is especially true if you’re trying to avoid spending an arm and leg for a house while ensuring your new neck of the woods isn’t a ghost town with a small jobs market and not much to do.

In many ways, the metros in our study provide the best of both worlds for homebuyers. They’re not necessarily as crowded, expensive or fast-paced as some of the country’s biggest cities, nor are they as low-key as many of the nation’s towns. Instead, they tend to offer various employment opportunities and housing options while not being prohibitively expensive.

Owing to this, these metros can be a good place for would-be buyers to consider in today’s expensive housing market where finding an affordable place to live can be challenging.

Tips for homebuyers

Even in areas generally friendly to homebuyers, purchasing a home can be difficult. Here are three tips that can make the buying process run a bit more smoothly.

- Remember: The lower your rate, the more you save. By shopping around for a mortgage before you buy, you can increase your odds of finding the best possible rate on a mortgage. This could help you lower your monthly payments and spend less in interest over your loan’s lifetime.

- Consider different mortgage options. While a conventional 30-year, fixed-rate mortgage might be the best option for some, it’s not for everyone. For example, loans with shorter terms — like 15-year mortgages — or ones backed by government agencies like the Federal Housing Administration (FHA) might be better for other homebuyers.

- Don’t stretch yourself too thin. Spending too much on housing costs can increase your risk of falling behind on other important bills or defaulting on your mortgage. While different households may have slightly different financial needs, trying to spend less than 30% of your monthly income on housing costs can help you keep on top of your bills without being overwhelmed.

Methodology

Data in this study comes from the U.S. Census Bureau 2021 American Community Survey with one-year estimates — the latest available at the time of writing. The six variables that make up the overall ranking were weighted equally. We chose them for the following reasons:

- Median home value: While other variables like income also play a major role in how affordable or easy it is to buy a house in a metro, areas with lower home prices can be more accessible to would-be buyers in today’s high-price/high-rate housing market.

- Homeownership rate: Higher homeownership rates can signify that homeownership is easier to attain than in areas where homeownership rates are lower.

- Median household income of owner-occupied homes with a mortgage: Higher incomes can make dealing with the costs associated with homeownership easier and less stressful.

- Median monthly housing costs of owner-occupied homes with a mortgage: Lower housing costs can leave homeowners with more wiggle room in their monthly budgets and more money to put into savings.

- Share of owner-occupied homes with a mortgage that spend less than 30% of their monthly income on housing costs: Households that spend less than 30% of their monthly income on housing costs can have an easier time staying on top of things like their mortgage payments, as well as the costs associated with regular maintenance.

- Median annual property taxes for homes with a mortgage: Lower property taxes can signify that an area is more affordable.